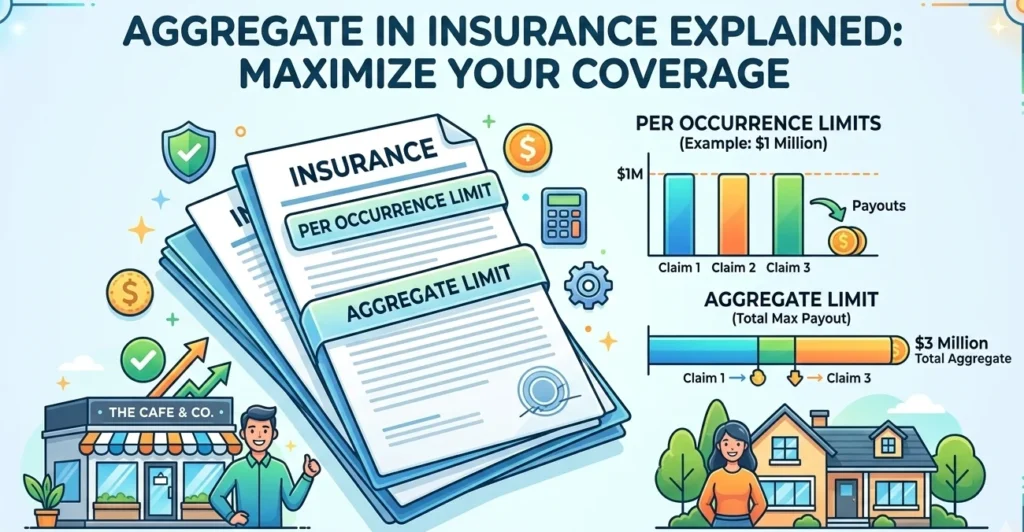

In insurance, aggregate refers to the total maximum amount an insurance policy will pay for all claims during a policy period.

It is essentially a cap on the insurer’s total liability, ensuring that claims are covered up to a specified limit, after which the policyholder is responsible for any additional costs.

Aggregate limits are a standard feature in commercial liability policies, homeowners insurance, and other property/casualty policies. Understanding this term is crucial for policyholders who want to know how much protection their insurance truly provides.

Understanding Aggregate in Insurance

Insurance can be complicated, and terms like aggregate often confuse new policyholders. Let’s break it down in simple terms:

- Single Claim Limit: The maximum an insurance policy pays for a single event or claim.

- Aggregate Limit: The maximum an insurance policy pays for all claims combined during the policy term, usually one year.

For example, if a business has a general liability policy with a $1,000,000 per occurrence limit and a $2,000,000 aggregate limit, this means:

- Each separate incident can be paid up to $1,000,000.

- The total of all incidents in a year cannot exceed $2,000,000.

Aggregate limits protect insurers from unlimited payouts, while informing policyholders about the maximum financial safety net their policy provides.

Origin and Popularity of Aggregate Limits

Aggregate limits became standard in insurance during the 20th century as commercial liability risks increased. Before aggregate limits:

- Insurers risked unlimited payouts in catastrophic scenarios.

- Businesses often faced uncapped liability exposure, making insurance premiums extremely high.

With the introduction of aggregate limits:

- Insurers could balance risk and set predictable premiums.

- Policyholders gained clarity on total coverage over a policy period.

- The concept became particularly popular in general liability, commercial umbrella, and workers’ compensation policies.

Today, aggregate limits are widely used because they provide both financial protection and risk management transparency.

Types of Aggregate Limits

Insurance policies may have different types of aggregate limits. The main types include:

| Type | Description | Example |

|---|---|---|

| General Aggregate | Maximum payout for all claims except certain exclusions | $2,000,000 aggregate on a business liability policy |

| Products-Completed Operations Aggregate | Maximum payout for claims related to products or completed services | $1,500,000 for product liability incidents |

| Per Policy Aggregate | Single maximum limit for all claims under one policy | $3,000,000 for a commercial liability policy |

| Per Project or Per Location Aggregate | Specific limit for claims tied to a project or property | $500,000 for one construction site in a builders’ risk policy |

Knowing which aggregate applies helps policyholders manage risk more effectively.

How Aggregate Limits Work in Real Life

Let’s use a practical example to illustrate:

Scenario:

A small construction company has a general liability policy with:

- $1,000,000 per occurrence limit

- $3,000,000 general aggregate limit

During the year, the company faces three separate claims:

- A slip-and-fall incident costing $900,000

- A property damage claim costing $1,200,000

- A lawsuit for defective workmanship costing $1,500,000

Calculation:

- First claim: $900,000 → covered fully

- Second claim: $1,200,000 → $1,000,000 per occurrence limit → $1,000,000 covered

- Third claim: $1,500,000 → $1,000,000 per occurrence limit → $1,000,000 covered

Total payout: $900,000 + $1,000,000 + $1,000,000 = $2,900,000

Aggregate limit: $3,000,000 → remaining coverage: $100,000

Any additional claim beyond the $3,000,000 aggregate would not be covered, leaving the company responsible for the balance.

Why Aggregate Limits Are Important

Aggregate limits are not just a technical detail—they directly affect financial protection:

- Budgeting: Helps businesses understand how much insurance they actually have.

- Risk Assessment: Allows businesses to evaluate if the aggregate is sufficient for high-risk operations.

- Premium Calculation: Higher aggregate limits typically lead to higher premiums.

- Avoiding Gaps: Policyholders may buy umbrella or excess policies to extend aggregate coverage if needed.

Without understanding aggregate limits, a policyholder might assume full coverage for multiple claims, only to discover the policy cap has been reached.

Common Examples of Aggregate Limits in Insurance

| Insurance Type | Typical Per Occurrence Limit | Typical Aggregate Limit | Notes |

|---|---|---|---|

| Commercial General Liability | $1,000,000 | $2,000,000 | Most standard business liability policies |

| Homeowners | $300,000 | $500,000 | Covers property and liability claims in one year |

| Auto Liability | $500,000 | $1,000,000 | For fleet vehicles or commercial cars |

| Umbrella Policy | $1,000,000 | $5,000,000+ | Adds extra coverage beyond primary policies |

Understanding these limits helps avoid underinsurance, especially for businesses with multiple exposure points.

Aggregate vs Per Occurrence Limits

Many policyholders confuse aggregate limits with per occurrence limits. Here’s a clear comparison:

| Feature | Per Occurrence Limit | Aggregate Limit |

|---|---|---|

| Definition | Max coverage per single incident | Max coverage for all incidents in the policy period |

| Example | $1,000,000 per lawsuit | $3,000,000 for all lawsuits in a year |

| Function | Protects against a single high-cost claim | Protects against multiple claims accumulating over time |

| Importance | Ensures major incidents are covered | Ensures total claims don’t exceed policy capacity |

How to Maximize Your Aggregate Coverage

- Assess Risks: Evaluate your business or property exposure to determine if the aggregate limit is sufficient.

- Consider Umbrella Policies: If the aggregate seems low, an umbrella policy can extend coverage significantly.

- Review Policy Period: Aggregate limits reset annually; understand the coverage timeline.

- Separate Limits by Type: Some policies have separate product-completed operations aggregates—know which applies.

- Regularly Update Insurance: Growth in business or property value may require higher aggregate limits.

Alternate Meanings of Aggregate in Insurance

While “aggregate” usually refers to a policy cap, it can also mean:

- Aggregate Premium: Total premiums paid over multiple policies or insureds.

- Aggregate Exposure: The total risk exposure a company or insurer has at a given time.

In other industries, aggregate may simply mean “total” or “combined”, but in insurance, it’s always tied to limits or financial caps.

Real-World Example: Small Business Liability

Scenario:

A catering company has a general liability policy with:

- $500,000 per occurrence

- $1,000,000 aggregate

During the year:

- Client A suffers food poisoning → claim: $400,000

- Client B sues for property damage → claim: $450,000

- Client C sues for slip-and-fall → claim: $300,000

Outcome:

- First claim: $400,000 → covered

- Second claim: $450,000 → covered

- Third claim: $300,000 → only $150,000 covered (aggregate reached)

- Remaining $150,000 → out-of-pocket for the company

This shows why understanding aggregate limits is crucial for financial planning.

FAQs

What does aggregate mean in insurance?

It is the total maximum amount an insurance policy will pay for all claims during a policy period.

Is aggregate limit per claim or per year?

Aggregate limits usually apply per policy period, commonly one year, for all claims combined.

How does aggregate affect coverage?

It caps the total payout. Once the aggregate is reached, the policy stops paying, even if per-incident limits remain.

Can I increase my aggregate limit?

Yes, by purchasing higher coverage or adding umbrella/excess policies.

Do all insurance policies have aggregate limits?

No. Some policies, like basic personal auto insurance, may only have per-incident limits.

What happens if claims exceed the aggregate limit?

The policyholder is responsible for any costs beyond the aggregate limit.

Why is aggregate important for businesses?

Businesses face multiple claims each year. Aggregate limits protect insurers and help businesses plan financially.

Is aggregate the same as total coverage?

Yes, it represents the total coverage available in a policy period, though per-incident limits may restrict individual claim payouts.

Does homeowners insurance have aggregate limits?

Yes, often on liability coverage, to cap total payouts for the policy year.

Conclusion:

- Aggregate is a policy’s total payout limit for all claims in a policy period.

- It differs from per occurrence limits, which cap individual claims.

- Understanding aggregate helps businesses and individuals avoid underinsurance.

- Umbrella or excess policies can supplement low aggregate limits.

- Always review policy details to know how aggregate, per occurrence, and exclusions interact.

Aggregate limits are a critical part of insurance literacy, ensuring policyholders know the maximum protection they have and can plan accordingly.

Read More Related Articles:

- Meaning of Por in Spanish: Practical Examples for Everyday Speech In 2026

- Righteousness Means in the Bible: God’s Character For 2026

- What Does ISG Mean in Text? Context Explained in 2026

Neon Samuel is a digital content creator at TextSprout.com, dedicated to decoding modern words, slang, and expressions. His writing helps readers quickly grasp meanings and understand how terms are used in real conversations across text and social platforms.