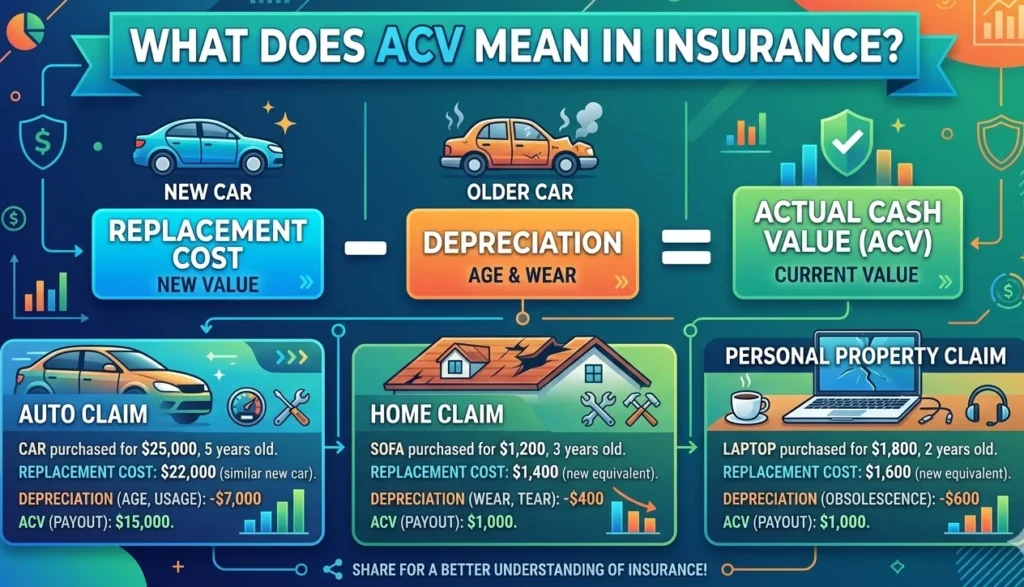

In insurance, ACV stands for Actual Cash Value. It refers to the replacement cost of your insured property minus depreciation.

ACV is commonly used in property, home, and auto insurance to determine how much an insurer will pay after a covered loss.

Understanding ACV is essential for homeowners, car owners, and renters. It can influence your claim payouts, coverage options, and decisions about repair or replacement. Let’s explore ACV in detail, its origin, usage, examples, and alternatives.

Origin and Popularity of ACV

The concept of ACV originated in property insurance to provide a fair method for valuing damaged or destroyed property. Insurers realized that paying full replacement cost for old or depreciated items was not economically sustainable.

- Early 20th century: Property and auto insurance policies began using depreciation-adjusted payouts to calculate losses.

- Popular usage today: ACV is standard in most homeowners’ and auto insurance policies, though some policies offer replacement cost value (RCV) as an alternative.

ACV became popular because it balances fair compensation for the insured while avoiding overpayment for aged or worn property.

How ACV Works in Insurance

ACV is calculated as:

ACV = Replacement Cost – Depreciation

Where:

- Replacement Cost is what it would cost to replace the property with a new one of similar kind and quality.

- Depreciation accounts for age, wear, and obsolescence of the item.

Example:

- Your 5-year-old laptop was destroyed in a fire.

- Replacement cost today: $1,200

- Depreciation: $400

- ACV payout: $1,200 – $400 = $800

In this case, ACV reflects the real-world value of your laptop at the time of loss, not what you originally paid.

Why ACV Is Used

ACV is used for several reasons:

- Cost control: Insurers avoid paying full replacement for old items.

- Fair valuation: Reflects actual value of property at the time of loss.

- Policy clarity: Provides transparency in claims for items with age-related depreciation.

However, some consumers prefer Replacement Cost Value (RCV) policies because ACV can result in lower payouts, especially for older items.

ACV vs Replacement Cost

It’s important to understand the difference between ACV and replacement cost:

| Factor | ACV (Actual Cash Value) | RCV (Replacement Cost Value) |

|---|---|---|

| Calculation | Replacement cost – depreciation | Full replacement cost |

| Payout Example | Laptop 5 years old: $1,200 – $400 = $800 | Laptop 5 years old: $1,200 |

| Depreciation | Deducted | Not deducted |

| Premium | Usually lower | Usually higher |

| Best for | Older items or cost-conscious policies | Full replacement coverage |

Friendly tip: ACV is often cheaper for insurance premiums, but may leave you paying out-of-pocket to replace older items fully.

ACV in Different Types of Insurance

1. Auto Insurance

In auto insurance, ACV determines the payout if your car is totaled or stolen:

- Example: A 10-year-old car valued at $8,000 before an accident:

- Replacement cost of a similar car: $12,000

- Depreciation: $4,000

- ACV payout: $8,000

Insurers often use market value, mileage, condition, and demand to calculate ACV for vehicles.

2. Homeowners Insurance

ACV applies to personal property like furniture, appliances, or electronics:

- Example: Your 7-year-old sofa is damaged in a fire:

- Replacement cost: $1,000

- Depreciation: $350

- ACV payout: $650

Buildings themselves are often insured with replacement cost coverage, but personal property may default to ACV unless upgraded.

3. Renters Insurance

Renters’ insurance often uses ACV for personal belongings:

- Clothing, electronics, and furniture are depreciated based on age.

- Older items will have lower ACV payouts than their replacement cost.

Pro tip: Review your policy carefully if you want replacement cost coverage rather than ACV.

Examples of ACV Calculations

Here’s a detailed table of typical ACV calculations:

| Item | Replacement Cost | Depreciation | ACV Payout |

|---|---|---|---|

| Laptop, 3 years old | $1,200 | $300 | $900 |

| TV, 5 years old | $800 | $400 | $400 |

| Sofa, 7 years old | $1,000 | $350 | $650 |

| Smartphone, 2 years | $900 | $150 | $750 |

| Car, 10 years old | $12,000 | $4,000 | $8,000 |

These examples show how depreciation reduces payouts under ACV. It’s always based on age, condition, and useful life of the item.

Factors That Affect ACV

Several factors influence ACV calculations:

- Age of the item: Older items have higher depreciation.

- Condition: Well-maintained items may retain more value.

- Market trends: Supply and demand can affect value.

- Type of insurance: Auto, homeowners, or renters policies may calculate differently.

- Local pricing: Cost of replacement in your area may influence ACV.

Pros and Cons of ACV

| Pros | Cons |

|---|---|

| Lower insurance premiums | Lower payout for older items |

| Reflects real-world depreciation | May not cover full replacement cost |

| Fair compensation for worn items | Can be confusing to policyholders |

| Simplifies claims process | May require additional out-of-pocket funds |

Friendly tip: ACV is more cost-effective for insurers and sometimes consumers, but it can leave gaps if you need full replacement of high-value, aged items.

ACV vs Depreciated Value vs Market Value

ACV is sometimes confused with other terms:

| Term | Meaning | Difference from ACV |

|---|---|---|

| Depreciated Value | Replacement cost minus accumulated depreciation | Essentially the same as ACV in most cases |

| Market Value | Current resale value of an item | Market value can fluctuate and may differ from ACV |

| Replacement Cost | Full cost to replace item without depreciation | ACV subtracts depreciation |

Understanding these differences helps prevent surprises during claims.

How to Increase Your ACV Payout

You can take several steps to maximize ACV payouts:

- Keep receipts and records for items.

- Maintain furniture, electronics, and vehicles in good condition.

- Consider upgrading to replacement cost coverage for high-value items.

- Document property with photos or videos.

- Work with insurers to understand depreciation schedules.

Practical Examples in Insurance Claims

| Scenario | Policy Type | Replacement Cost | Depreciation | ACV Payout |

|---|---|---|---|---|

| Fire destroys 3-year-old laptop | Homeowners | $1,200 | $300 | $900 |

| 10-year-old car totaled in accident | Auto | $12,000 | $4,000 | $8,000 |

| Apartment flood ruins 5-year-old sofa | Renters | $1,000 | $350 | $650 |

| Smartphone stolen, 2 years old | Homeowners/Renters | $900 | $150 | $750 |

Tips for Policyholders

- Review your insurance policy to see if ACV or replacement cost is applied.

- Keep records and receipts for valuable items.

- Understand how depreciation schedules affect ACV payouts.

- Consider endorsements or riders to upgrade coverage for high-value items.

- Ask your insurance agent questions about market vs actual cash value.

FAQs

What does ACV mean in auto insurance?

ACV is the amount your insurer will pay for a car after a total loss, based on current value minus depreciation.

Is ACV the same as replacement cost?

No. ACV subtracts depreciation, while replacement cost pays to replace the item with a new one.

Why is my ACV payout lower than the item’s price?

Depreciation reduces value over time; older items receive lower payouts.

Can I upgrade ACV to replacement cost coverage?

Yes. Many policies allow endorsements for personal property or vehicles.

Does ACV include taxes and fees?

Usually, ACV covers only the item’s value, not additional taxes or fees unless specified.

How is ACV calculated for a car?

It’s based on the market value, mileage, condition, and depreciation of your vehicle.

Is ACV used for homeowners insurance?

Yes, it applies to personal property like furniture, electronics, and appliances.

What’s the difference between ACV and market value?

ACV is depreciation-adjusted replacement cost, while market value is the resale price.

Do all insurers use ACV?

Most insurers use ACV for personal property, but replacement cost policies are also common.

Conclusion

ACV, or Actual Cash Value, is a fundamental concept in insurance that affects claim payouts, coverage decisions, and policy selection. By understanding ACV, you can make informed choices about homeowners, renters, or auto insurance and avoid surprises during claims.

Key takeaways:

- ACV = Replacement Cost – Depreciation

- Older or worn items have lower ACV payouts

- Replacement cost coverage is an alternative if you want full compensation

- Always review policies carefully and maintain records for high-value items

Understanding ACV ensures clarity, avoids frustration, and helps you get the most from your insurance coverage.

Read More Related Articles:

- “Le” Means in Spanish: Why This Small Word Matters So Much In 2026

- OP Meaning in Gaming – The Term Every Gamer Uses (2026)

- What Does QHS Stand For? A Clear Medical Definition In 2026

Luna Hartley is a content creator at TextSprout.com, where she specializes in explaining word meanings, modern phrases, and everyday language used in texts and online conversations. Her writing focuses on clarity and context, helping readers understand how words are actually used in real communication.